This post is written by Eliud Birachi, Mercy Mutua, Clare Mukankusi, Noel Templer, Louise Sperling, Patricia Onyango, Sylvia Kalemera, Robin Buruchara, Bhramar Dey and Jean Claude Rubyogo.

Common bean (Phaseolus vulgaris L.) plays a key role in the livelihoods of smallholder farmers in Tanzania as a food and nutrition security crop and a source of income for producers. It is the leading leguminous crop, accounting for 78% of land under legumes; and over 75% of rural households in Tanzania depend on beans for daily subsistence. Per capita bean consumption is 19.3 kg, contributing 16.9% protein and 7.3% calories in human nutrition and 71% of leguminous protein in diets. With its 1.2 million tons per year (2018), Tanzania is the top bean producer in Africa and seventh globally. More than a quarter of its beans are exported regionally to 10 neighboring countries and beyond. Common bean is identified as a focus crop in the Tanzania Agriculture Sector Development Programme II (ASDP) Phase II.

Yellow bean is one of the most traded bean types in Tanzania. However, there is limited information on its production and trade with potential negative implications on seed supply systems and other possible investments. S34D (led by ABC/PABRA) conducted a recent survey that shows existence of an established yellow bean corridor across Tanzania and the region (Burundi, DRC, Kenya, Rwanda, Uganda, Zambia). A huge market pull for the yellows exits in the eastern and southern Africa regions.

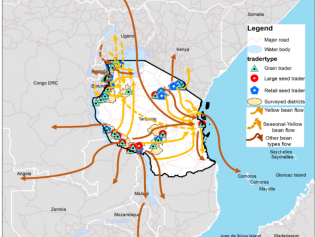

Using the Bean Corridor framework of the Pan-Africa Bean Research Alliance (PABRA) — a program facilitated by the Alliance of Bioversity International and International Centre for Tropical Agriculture (ABC) in collaboration with Tanzania Agricultural Research Institute (TARI) and Catholic Relief Services (CRS) — [1] conducted a survey of the yellow bean value chain in Tanzania from July through August 2019. The objective of the survey was to characterize and explore trade of yellow bean grain and potential seed markets.[2] The survey collected data samples from 298-grain traders (including wholesalers, exporters, aggregators, and retailers) and 64 potential seed traders (large and retail traders) from 12 regions across four administrative zones in Tanzania (Map 1). The survey also collected bean samples for DNA analyses.

The corridor is largely driven by informal seed supplies. However, the DNA assessments of samples collected from the traders in the markets showed that about 60% of the informally traded yellow beans are derived from modern varieties released in Tanzania. These varieties were injected into the informal seed systems through wide-scale, on-farm demonstrations followed by multiplication by specialized decentralized seed producers and farmers themselves. The diffusion happens via routine local market sales, and by grain traders moving the varieties across longer distances driven by high market demand. The informal nature of the trade means that traders and retailers jointly handle informal seed supplies and grain trade.

Key Results

- There are ample business volumes; a small sample of about 300 traders handled more than 40,000 MT of yellow bean over previous 12 months (with this being only a fraction of the total trade).

- There are strong perceptions on the quality of yellow bean varieties linked to their source. The preferred yellow beans in Dar es Salaam and other markets are a relatively large-sized, round and yellow variety generally referred to as “Gololi”, meaning round shaped. This is one of the released varieties and is known also by its research name, Selian 13. As an example, yellow beans from the Northern Zone and Tanga region are considered of superior grain quality due to their relatively short cooking time, minimum flatulence and good palatability. Subsequently the consumers pay higher (25% than the next yellow bean varieties); while those from Kagera are considered as low-quality beans by markets in Dar es Salaam.

- DNA results showed that the majority of the Gololi beans were in fact a released variety Selian 13. However, some (13.2%) of the “Gololi”- looking bean genotypes (collected by TARI from the market and included in the reference set) were in fact a landrace from Uganda, Masindi yellow. Furthermore, 50% of the traded varieties were officially released in Tanzania (Selian 13, Njano Uyole and Uyole 98). The rest either were derived from neighboring countries or could not be clustered. In addition, the most traded varieties were also of the released types. Despite the diversity in the yellow beans, there are clear preferences of varieties by traders and consumers.

- The seed of these modern yellow bean varieties were injected in the informal seed systems via a sequence of actions, catalyzed by the formal research sector. There was widespread on farm popularization by TARI/ABC-PABRA carried out before and after release of these varieties, leveraging organized farmer groups in the bean corridors. Also, there was limited decentralized Quality Declared Seed (QDS) production. The varieties were then diffused at large scale by farmers growing the seed and selling harvests in local markets, and larger traders moving these welcomed varieties across Tanzania and multiple African regions.

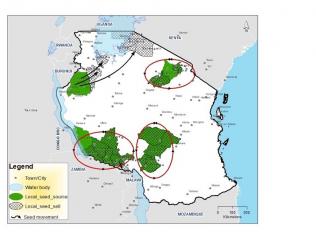

- To respond to huge demand for yellow bean seed, traders have organized a vibrant informal (potential) seed supply in the bean corridors. These traders double up as seed suppliers and provide avenues for strengthening the seed supply system in the corridor. The geographic sourcing of seed and grain is quite distinct — seed source and sale tends to be much within the region (near where local seed is planted). For grain, source, and especially sale, is much more far-reaching (Map 1). The local (within region) circulation of seed is particularly striking when maps of seed flows alone are charted (Map 2).

- According to traders, the peak selling seed periods coincide with planting time. September to December reflect the peak selling periods, when prices are also highest for the beans. Farmers are paying 25% for the potential seed of Njano Golori than other bean varieties

- Women dominate retail trade in the yellow bean, while men dominate export and aggregation businesses. Women sold closer home within the district; similarly, they mainly sourced grain close to their localities while men tended to source and sell in distant regions or regional markets.

- Traders did not prefer to sell mixed beans, but rather preferred single varieties as they fetched up to 50% higher (Photo 1). Discoloration of some of the beans when stored for longer periods posed a significant challenge to traders — as beans, which retained original color, were always preferred. Other key constraints were the way the markets were organized and trade levies when moving grain internally from one district to another.

-

Map 1: Overview of trader grain and seed flows (all samples)

Map 2: Zones of Sourcing and Selling Potential Seed

Various yellow beans and their prices in Dar es Salam market

- Recommendations:

- Traceability in the yellow bean corridor is necessary, especially for informal seed supply but also for closer linkages between aggregators and grain producers. Most traders expressed interest for support to connect to each other via digital means as part of yellow bean corridor strengthening in Tanzania. Digital payment solutions via the system of aggregators is one such possibility to support the development of the value chains.

- The yield of yellow bean in Tanzania is low. This poor yield can be increased through demand-led breeding of high yielding/climate-smart and market-preferred varieties supported by more efficient seed delivery systems.

- Differentiated bean markets (various varieties) are an obvious driver of seed demand through which integrated seed system (combing both formal and informal) is the sustainable way to ensure seed access. However, deliberate efforts must be put into creating working linkages between the bean traders and seed/grain producers.

- Additionally important are linkages with traders-led bean business platforms; enablers through the policy environment, management ,and business training/support to the traders; agronomic practices to farmers; and significantly, enhancing the quality of the seeds in the current informal seed system in the wider yellow bean corridor.

- The yellow bean study showed the regionality of bean trade and exchange; thus its upgrade can only be tackled within the regional Bean Corridor framework.

Concluding remarks about the yellow bean corridor and investments opportunities

Informal seed systems play a major role in linking demand and supply for yellow beans in Tanzania and the region. These systems can be strengthened to improve the quality of potential planting seed and increase the yield of the yellow beans. Therefore, there is a need to improve linkages between NARS/breeding programs with traders and seed companies to increase their participation.

There is a major role for the traders to disseminate new varieties that are climate-smart, disease-resistant, high-yielding, etc. The traders move large volumes (as evident in our survey). But these traders (like any other seed system actor) needs greater capacity strengthening. Their potential can be better realized by investing in sufficient provisioning of varietal information to potential users; increasing their technical capacities to handle the beans linkages with formal seed systems and seed quality; increasing collaborations and linkages in the value chain; and providing sufficient policy support for within and cross border trade.

Strengthening local supplies and local seed systems will help communities and households to absorb shocks and adapt and build resilience in stress conditions (such as Covid-19 pandemics). When mobility is restricted, strong and resilient local endeavors can support with continual supply of quality planting materials.

This article was first published on www.agrilinks.org